In the rapidly evolving landscape of drug discovery and development, biosimulation has emerged as an indispensable tool that stands at the intersection of computational science, biology, and pharmacology. As pharmaceutical companies and biotech firms strive to accelerate the development pipeline, reduce costs, and improve safety outcomes, biosimulation offers a promising pathway to achieve these objectives through sophisticated in silico modeling. The biosimulation market is expected to witness strong growth, led by increased demand for precision medicine, regulatory approval, and technological innovation.

Market Overview and Key Drivers

The biosimulation market, which encompasses software solutions, consulting services, and integrated platforms, is on the cusp of exponential expansion. The global biosimulation market size was estimated at USD 3,910.0 million in 2024 and will reach USD 4.57 billion in 2025 and is expected to reach USD 10,005.0 million by 2030, growing at a CAGR of 17.0% from 2025-2030. This growth trajectory reflects increasing adoption across pharmaceutical research, biopharmaceuticals, and personalized medicine sectors.

Several factors underpin this optimistic outlook. First, regulatory bodies like the FDA and EMA have started incorporating biosimulation data in the approval process and highlighting its potential to downsize and shorten clinical trials. Second, computational capacities, machine learning algorithms, and big data analytics have greatly improved the accuracy and relevance of biosimulation models. Third, increasing interest in personalized medicine and targeted therapy requires more accurate predictive tools, further driving market expansion.

Moreover, the complexity of biologics and gene therapies is growing, requiring new modeling strategies to forecast pharmacokinetics, pharmacodynamics, and immunogenicity. Consequently, biosimulation is evolving from an ancillary tool to a key element in drug development pipelines.

Product Segments and Technological Trends

The biosimulation market can be extensively divided into software solutions and services. Software solutions encompass simulation platforms supporting pharmacokinetic/pharmacodynamic (PK/PD) modeling, physiologically based pharmacokinetic (PBPK) modeling, and systems biology simulations. Services consist of consulting, model validation, regulatory submissions, and custom development.

Recent technological trends are driving innovation across such segments. Machine learning and artificial intelligence algorithms are incorporated into biosimulation platforms to improve predictive validity and automate sophisticated modeling processes. Cloud computing enables scalable, shared modeling environments available to stakeholders all over the globe, promoting transparency and efficiency.

The use of digital twin technology, where virtual copies of biological systems or organs are created, is picking up pace, allowing patient-specific simulations for precision medicine. Also, the incorporation of real-world data (RWD) from electronic health records and wearable devices enhances model inputs, enhancing the relevance and validity of simulations.

Market Segmentation and Application Areas

The market for biosimulation serves various applications throughout the lifecycle of drug development. The most significant segment is drug discovery and preclinical research, where biosimulation allows virtual screening of compounds, toxicity prediction, and optimization of drug candidates. This minimizes dependency on expensive and time-consuming lab experiments.

In clinical development, biosimulation is critical in the selection of dose, optimization of trial design, and biomarker identification. Biosimulation aids regulatory approvals through the supply of solid in silico evidence for safety and efficacy, which shortens approval timelines.

In personalised medicine, biosimulation models are customised to individual patient information, enabling clinicians to make more precise predictions of drug action and adverse effects. This use case is especially relevant in oncology, neurology, and rare disease treatment, where patient heterogeneity requires nuanced treatment approaches.

Regional Market Trends (2024–2030)

-

Biosimulation Market in North America

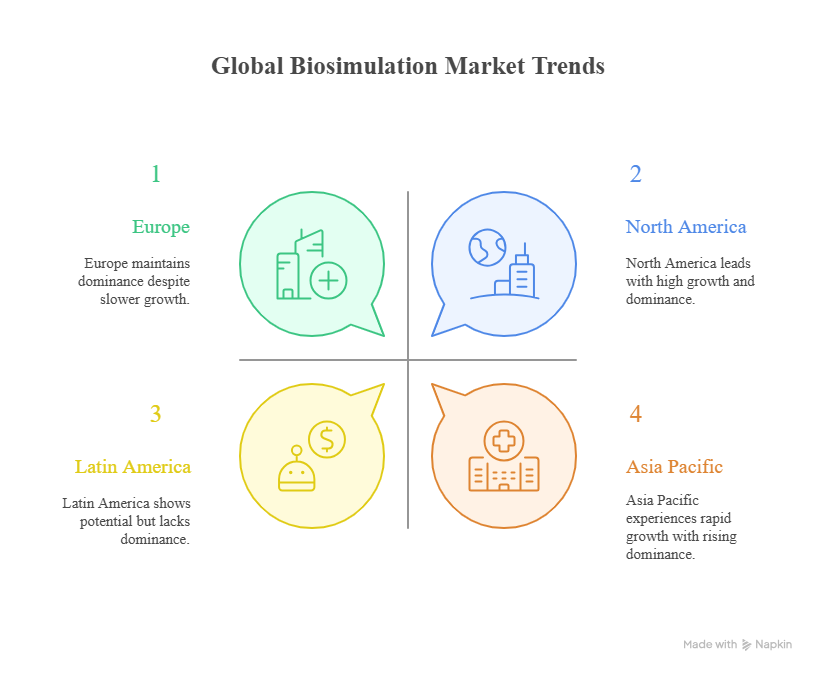

North America continues to dominate the biosimulation industry, accounting revenue share of 49.90% in 2024. The dominance of this region is attributed to strong investments in pharmaceutical R&D, well-established healthcare infrastructure, and forward-looking regulatory landscapes that readily embrace and incorporate biosimulation data in the approval process of drugs. Emerging technologies like machine learning-based models and digital twin applications are especially leading the charge in North America. The regulatory bodies of the country, such as the FDA, have also started to include biosimulation data in drug approval, speeding up adoption further.

-

U.S. Biosimulation Market Trends

The U.S. biosimulation market is on the leading edge of technology development and regulatory approval. The FDA’s changing guidelines, such as the application of model-informed drug development (MIDD), are instrumental in influencing market expansion. The nation’s heavy investments in precision medicine and biologics development are driving the need for sophisticated biosimulation technologies that assist in dose prediction, patient stratification, and optimization of clinical trials.

The key player in the United States focuses on incorporating AI with traditional biosimulation platforms to enhance predictive accuracy and facilitate smoother drug approval pipelines. The surge in partnerships between biotech companies and digital health companies indicates that the nation is bent on transforming traditional R&D frameworks. Analysts foresee double-digit growth in the U.S. market, considering the growing demand for quicker timelines of developments and cost-effective solutions.

-

Europe Biosimulation Market Trends

The biosimulation market in Europe is dominated by fast uptake, aided by strict regulatory needs and a high focus on personalized medicine. The European Medicines Agency (EMA) has actively encouraged the use of modeling and simulation methods, viewing them as crucial to contemporary drug development.

Germany, the UK, and France are prominent European regions, with major investment in biotech innovation centers and cooperative research programs. The incorporation of biosimulation into clinical development and regulatory filing has resulted in higher uptake, particularly in intricate biologics and biosimilars. Market expansion in Europe occurs due to the rising take-up of digital twin technology and real-world data integration that improves predictive value.

-

Asia Pacific Biosimulation Market Trends

The Asia-Pacific region is anticipated to witness the highest growth rate in the biosimulation industry. This rapid growth is driven by expanding healthcare infrastructure, rising R&D investments, and supportive government policies aimed at fostering innovation in pharmaceuticals and biotech. For instance: In September 2024, Certara, Inc. a Imodel-informed drug development company, is expanding its Certainty client event with one-day conferences in China, South Korea, and Japan this September. The APAC region has been a hub for drug discovery and development accounting for $210 billion in the pharmaceutical market in 2023. Certara’s Certainty catalyzes innovation through collaboration, providing attendees with lessons from experts in biosimulation, data analytics, and regulatory science.

China, Japan, and India are the most important markets in the region. The Japan biosimulation market generated the highest share of revenue in the Asia Pacific market due to technological advancements and strategic plans by industry players to drive innovation by creating innovative biosimulation tools. The biosimulation market size in China is expected to grow in the forecast period, as the focus on personalised medicine increases and more alliances and partnerships are created to implement biosimulation technologies.

-

Latin America Biosimulation Market Trends

Throughout the forecast period, the market for biosimulation in Latin America is slated to grow at a significant CAGR. Contributing to this are increasing public interest and investment in artificial intelligence (AI) systems, along with increasing healthcare and biotech industry uptake of these systems.

-

Middle East and Africa Biosimulation Market Trends

The Middle Eastern and African biosimulation market size is expected to advance at a high CAGR through the forecast period. Increasing healthcare expenditure, drug development processes, and favorable government policies are all primary drivers.

Market Drivers and Challenges

The increasing use of biosimulation is mainly triggered by regulatory acceptance of simulation and modeling data as part of the approval process. Agencies are now more accepting of these models as key tools for proving drug safety, efficacy, and optimal dosing, particularly in intricate biologics and gene therapies. The industry’s move toward personalised medicine further increases patient-specific model demand, which enhances clinical results and lowers adverse events.

Cost savings continue to be a key driver. Conventional drug development is expensive and time-consuming; biosimulation presents a way to expedite workflows, minimize failures, and decrease timelines, resulting in significant cost savings. The COVID-19 pandemic hastened these movements, proving the efficacy and advantages of remote, digital-first research.

Yet there are challenges. Standardisation and quality of data are still some of the concerns. Data heterogeneity, differences in modeling practices, and issues related to model validation prevent regulatory acceptance on a broader scale. Maintaining security and privacy of data, especially when consolidating real-world data, is another top obstacle industry participants need to tread cautiously.

Interoperability problems among various modeling platforms and requirements for skilled individuals well-versed in biology and sophisticated data analytics further impede progress. Implementing industry-wide standards and developing the capabilities of the workforce are key steps toward transcending these hurdles.

Conclusion

The biosimulation industry stands at the threshold of a revolutionary period characterised by technology convergence, regulatory approval, and a developing concept of personalized therapy. Revolutionising clinical trial data from conventional laboratory testing to dynamic, in silico models presents unprecedented opportunities for optimising drug development efficiency, enhancing patient safety, and saving costs.

Despite these challenges, the journey forward involves surmounting large obstacles pertaining to data quality, standardization, and regulatory approval. All stakeholders across the industry will have to work together to create holistic standards, drive technology innovation, and encourage upskilling of the workforce. As the industry progresses, incorporation of biosimulation into traditional drug development will radically transform the discovery, testing, and launch of new treatments.

Embracing this digital transformation in biosimulation will eventually speed the bringing of new medicines to market, so patients everywhere can enjoy safer, more effective medicines with reduced development times and improved outcomes. The biosimulation industry’s future holds a smarter, more responsive model for medical innovation—guided by data, fueled by technology, and focused on human health improvement.

{kind=link}